Once you have built your retirement corpus, the next logical step is figuring out how to make it last a lifetime, ensuring that it meets all your financial goals. Retirement planning provides a disciplined approach to this problem.

Looking 25-30 years into the future, to create a retirement plan, is nothing short of crystal gazing! There is certainty of expenses and uncertainties with the returns that the corpus can provide with.

An ideal plan needs to consider multiple factors to improve its accuracy.

Factors Impacting the Calculations in a Retirement Plan:

Retirement planning depends on multiple internal and external factors. There may be a reasonable control over the internal factors, like the withdrawal rate itself. However, the external factors like the returns on investment are dependent on the markets. One can only rely on the long term expectations to estimate their impact on the plan.

The details of the factors are as below.

The Withdrawal rate: How much you want out of your corpus as retirement income is of course the most important factor. A lower withdrawal rate means less pressure on the portfolio and more opportunity for it to grow. Many investors misjudge this as the absolute return on the portfolio, i.e. if the portfolio returns 8% annually, it seems logical to be able to consume the entire 8% that year. However, that has a serious implication on the future inflation adjusted withdrawals. Similarly, if the portfolio does exceptionally well during the year, it should not be a trigger to increase the withdrawal rate

Many studies included the celebrated paper by William Bengen pegged a safe rate at 4%. The study was based on the US markets between 1926-1976. Few studies have increased this rate marginally and others had a lower recommendation.

Expected Rate of Return: This is a critical factor heavily dependent on the economic conditions and the chosen asset allocation strategy. Your ideal split between risk assets (like equity) and debt depends on multiple variables, including your risk tolerance, planned horizon and importantly the ability to take market impact.

It is natural to feel the urge to protect your hard-earned savings when you retire from the vagaries of markets. However, this often leads to a conservative bias, where one might move everything into debt to avoid the stress of market swings. But that would risk having a portfolio that doesn’t give inflation protection especially when the withdrawal from the retirement corpus can have a horizon of as long as 25-30 years.

Equity not just provides growth to the portfolio but the variability of its returns reduces significantly over long term. It is the only asset class that has consistently outpaced inflation over long periods. It acts as a shield against the rising cost of future withdrawals. So, it will be a mistake not to invest part amount in equity.

Having excess of equity can increase the expected returns but can overly expose the portfolio to the volatility of the markets.

Inflation Expectations: High inflation can severely compromise a retirement plan. Inflation works against the purchasing power of the income. Optically it is also dangerous, as it’s long-term impact is difficult to imagine.

An expense of Rs. Rs. 20 Lac annual would inflate by over 3 time by the end of 25 years, something that in general beats our imagination.

Categorizing your budget into critical (living expenses, medical, etc.) and discretionary (travel, dining out, etc.) expenses can provides a vital lever to control outflows during periods of high inflation. For example, a plan where critical expenses comprise 80% of total outflows is far more vulnerable to inflation shocks than one where they account for only 60-70% of the total expenses.

Plan Duration: This is a straightforward but essential variable. It is prudent to plan for a lifespan of 80 to 85 years. When planning for the future, couples should account for the age gap and differing life expectancies. On average, women outlive men by approximately five years.

Investment Volatility: While assuming linear returns simplifies calculations, real-world volatility—especially in equities—introduces uncertainty. Over the long run, equity adheres to the mean; a few years of poor or negative returns are often offset by higher returns in subsequent years. Since retirement planning is typically for a long period of time, investments do adhere to the mean returns.

Volatility is not just limited to equity. There are risks in debt investments too. The investments are prone to changes in interest rates and some may have credit risk too.

Experiencing a period of poor returns early in retirement negatively impacts the success rate far more than if the downturn occurs toward the end of the plan. Therefore, a good plan should test the impact of multiple market scenarios on the ability of the corpus to serve future cashflows.

Consumption of Principal: The choice between preserving the principal for heirs or systematically consuming it fundamentally dictates the sustainable withdrawal rate.

Confidence Level: The probability of success (based on historical data) determines the confidence level. A “100% certainty” comes at a high price. It requires a ultra-conservative withdrawal rate that could lead you to underspend and miss out on experiences you can actually afford. Ultimately, a great retirement requires a shift in mindset: moving from total risk avoidance to taking the calculated risks necessary to enjoy your wealth.

Other Goals: Retirement plans are unique, often involving cash outflows and inflows. A personalized plan should incorporate specific post-retirement goals and expected cash infusions to carve out a more accurate path. Risks related to health need to be covered through insurance.

These factors do not always work individually. They may appear independent but have a leading or lagging impact on each factors.

Understanding a Plan:

Let us take an example of Ajay with a Rs. 5 Crores retirement corpus who wants to decide his retirement strategy . Ajay is 55 and want to plan for 80 years.

A simulation of his situation with different Asset Allocation strategy gives the following results.

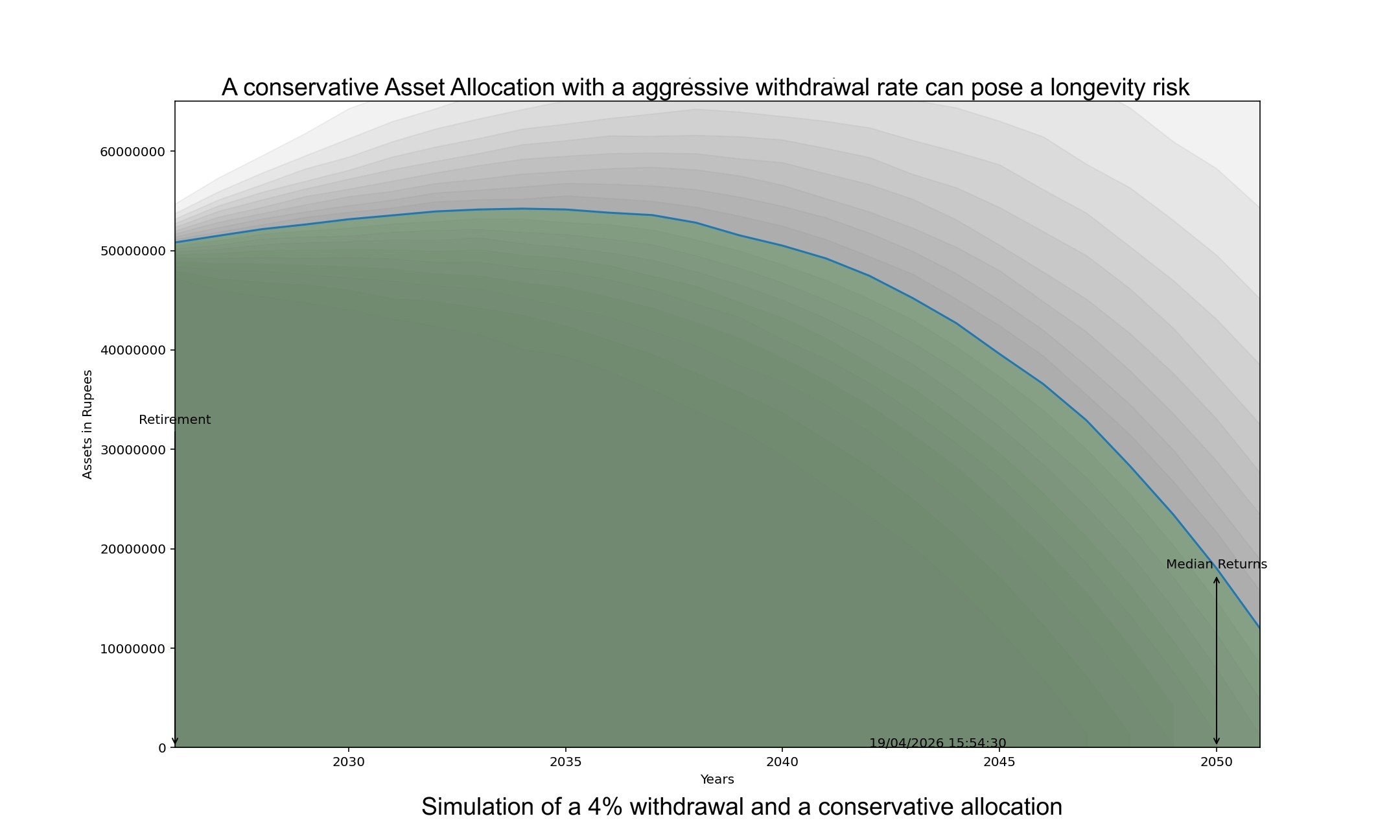

A conservative asset allocation approach with an Equity exposure of 20%.

| Annual Withdrawal Rate | Probability of Plan Success | Years the corpus is likely to survive after 25 years | Remarks |

| 4% | 96.53% | 1 | Prone to risk in case of prolonged underperformance of the markets |

| 3.50% | 99.39% | 6 | On Track |

| 3% | 99.96% | 12 | On Track |

A conservative approach for Ajay makes it more certain in terms of the probability of achieving but only works with a lower withdrawal rate. The success probability increases significantly as the withdrawal rate reduces. The strategy poses longevity risk especially in the 4% and 3.5% withdrawal rates.

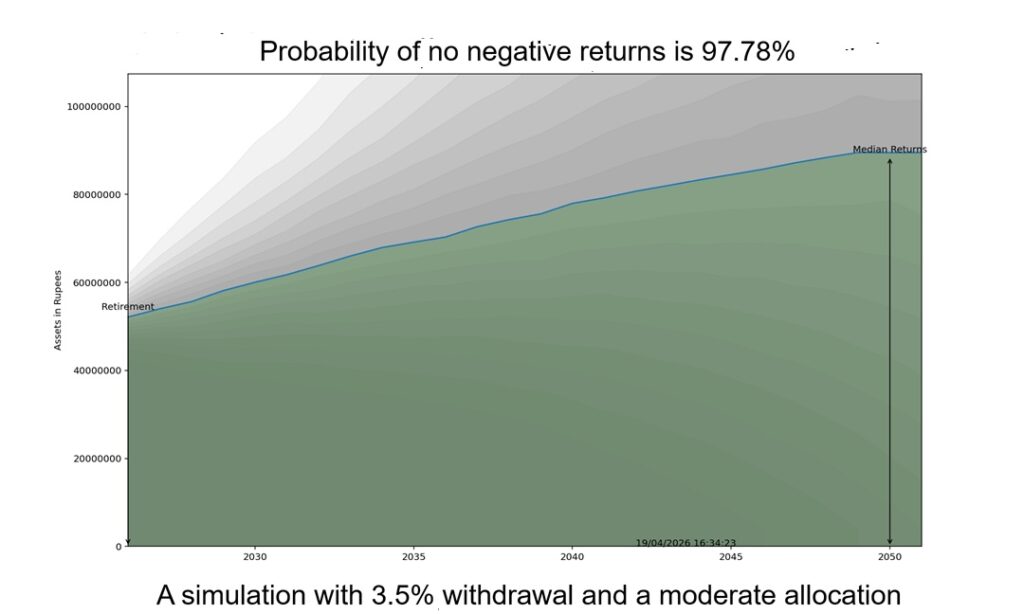

A balanced asset allocation approach with an Equity exposure of 44%.

| Annual Withdrawal Rate | Probability of Plan Success | Years the corpus is likely to survive after 25 years | Remarks |

| 4% | 95.59% | 5 | Prone to risk in case of prolonged underperformance of the markets |

| 3.50% | 98.33% | 12 | On Track |

| 3% | 99.57% | 20 | On Track |

Balanced approach also works well in the 3.5%-3% withdrawal rate. However, a 3% looks conservative as residual corpus is almost for 20 years.

A moderately aggressive asset allocation approach with an Equity exposure of 56%.

| Annual Withdrawal Rate | Probability of Plan Success | Years the corpus is likely to survive after 25 years | Remarks |

| 4% | 95.16% | 8 | Prone to risk in case of prolonged underperformance of the markets |

| 3.50% | 97.78% | 15 | On Track |

| 3% | 99.01% | 23 | On Track |

A moderately aggressive strategy marginally decreases the probability of achievement but at the same time also decreases the longevity risk. This is no surprise as more equity portfolio increases the volatility but has a higher return expectation overall. A withdrawal rate of 3.5% and 3% works well in terms of meeting the objectives as well as covering the longevity risk.

Conclusion & Study Findings:

Asset Allocation: The change in asset allocation across a specific withdrawal rate does not significantly alter the probability of achievement of the strategy. It has higher impact on the longevity risk. Being too conservative can lead to smaller residual portfolio and heighten longevity risk.

The Withdrawal Strategy: Across different allocations, a 4% rate-maintained success rates above 95%. However, the success of this strategy may get impacted due to prolonged underperformance of the markets or a sequence of market underperformance during early years. A 3.5%-3% withdrawal proved to be a much safer rate. None of the simulations turned negative up to the 80th percentile.

The Risk Strategy: The risk strategy also depends on the retirement demand. If Ajay can live on 15 Lac of annual retirement expenses (3% of 5 Crores), he can take higher risk with his allocation, reduce longevity risk and enjoy a higher success rate.

This is a simplistic view of a retirement plan which considers only fixed and regular payouts. There can be bullet expense, like home renovation etc and lumpsum cash inflows like maturity of a deposit that need to also be accounted for. There could also be unforeseen expenses like medical expenses that can impact the plan.

Retirement should mean financial freedom. But managing finances during this stage can be complex. A retirement plan can help reduce uncertainties and create sustainable income so that you can focus on things that matters the most to you.

Disclaimer: The study is based on long term capital market expectations and other statistical indicators. The results are based on a Monte Carlo simulations and on various assumptions. The simulation considers a normal distribution. This study should not be construed as an advice. Probability of Plan Success is calculated as negative portfolios with 2500 simulations over 25 years. A plan is considered as ‘On Track’ if no negative portfolio was observed above 80th percentile. The asset allocation also comprises debt, gold (5%)and liquid(5%) over the equity allocation. “Years the corpus is likely to survive after 25 years” is the expected corpus considering median returns divided by the inflation adjusted annual expenses. It does not consider inflation adjusted expense post 25 years. The results of a simulation can differ with every simulation that is run. This content is a property of Vasupradah Investment Advisory Services Limited and permission should be taken to quote.